How to Start Investing In a Big Way

Women are the top three financial advisers and the highest net-worth investors in the U.S. There's a reason for that – women have more money than men. They make better money managers because they can

Read More

Women are the top three financial advisers and the highest net-worth investors in the U.S. There's a reason for that – women have more money than men. They make better money managers because they can

Read More

With the majority of the public present on social media today, it is no wonder that businesses are using the platform to their advantage, and rightly so. Unlike other forms of marketing, using a social

Read More

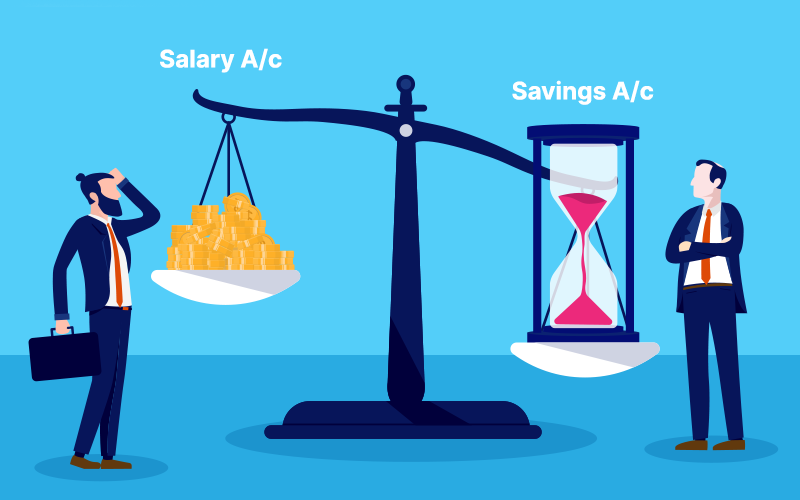

In today's fast-paced world, managing finances can be a challenging task. One common dilemma that many individuals face is whether to keep their salary account and savings account separate. While it may seem convenient to

Read More

In most groups, the financial institution is like Rodney Dangerfield: it receives no admiration. When the commercial enterprise is ideal, different humans take the credit. When business heads south, finance gets the blame. After all,

Read More

There are plenty of reasons to want a financial management program. First, keeping your finances all in one place allows you to see how you save and spend money easily. This way, you can make

Read More

Financial institution Indonesia (BI) announced its Wide Info plan lately to trouble waqf (Islamic endowment) based totally bonds as a social welfare mechanism to aid struggling business property. The first-class thing in finance Very catalog

Read More

It commenced life as remove from a massive public corporation; it then went wooing, unsuccessfully, because it became a unique cause acquisition enterprise. Until Tuesday, shareholders of ECN Capital must have felt like no one

Read More

The Reserve Financial Institution of India (RBI) is operating on a framework for standardizing inexperienced bond issuances and financing problems to align India with other nations with such regulations consistent with assets. Finance Framework RBI

Read More

Lured by using low-interest prices, low gasoline prices, and a crop of seductive vehicles that are quicker, smarter, and greener than ever, American drivers are increasingly driving in fashion. Don't be fooled by using the

Read More

MSME working capital loan is a credit option offered by financial institutions to start-ups, small companies, individual entrepreneurs, self-employed professionals, etc. This option allows businesses/individuals to mitigate daily operational and financial expenditures like account payable

Read More